Colsa Insurance Agency, Inc. Blog |

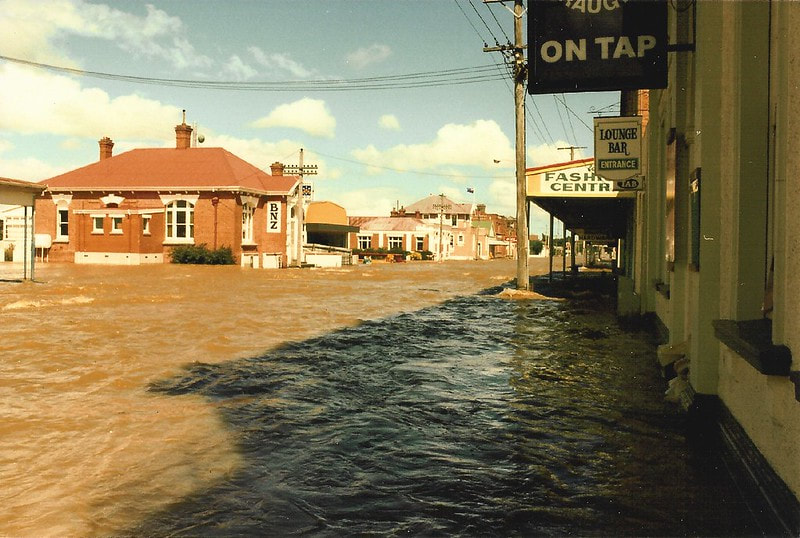

Almost everyone has a risk of their home being flooded, regardless of where they live. And now as flooding has become an annual threat to many communities across the country, even areas that were not considered flood-prone are also at risk. There was record rain and snow in many parts of the country in the early part of the year, and many areas can therefore expect flooding. According to the Federal Emergency Management Agency, more than 20% of all flood insurance claims come from areas outside of high-risk flood zones - and that number is rising with each passing year. That still means the vast majority come from high-risk areas. How can a property owner find out what their flood risk is? Gauging your flood risk FEMA considers a property to be at high risk of flood if there is at least a one-in-four chance of flooding during the life of a 30-year mortgage. Geographic areas with this risk are known as special flood hazard areas (SFHAs). Federal regulations require federally regulated or insured mortgage lenders to confirm that mortgaged properties in these areas carry flood insurance. The traditional way to determine a property's flood risk is to locate it on a flood insurance rate map (FIRM). FEMA publishes these maps based on geographic survey data. They are the official depictions of flood hazards in a locality. FIRMs are freely available for review at the Flood Map Service Center on FEMA's web site. As a property owner, you can view your flood risk by entering your address in the search field. Flood maps assign each area in a community to labeled flood zones. Areas with low-to-moderate risks of flooding are assigned to zones with labels beginning with the letters B, C, X or a shaded X. SFHAs are designated with the letters A or V. These areas are shaded on the maps for easy identification. Property owners can also search for their flood risks at FEMA's flood insurance consumer web site, www.floodsmart.gov. By entering your address in the fields on the home page, you can quickly learn whether you face a low-to-moderate or high risk. The site offers other valuable tools, such as an estimator that can calculate how much financial damage a given amount of water (two inches, four inches, etc.) would cause in homes of various sizes. For example, six inches of water in a 2,000 square foot home would cause $39,150 in damage. FEMA also offers a suite of flood risk products that go beyond the information provided in a FIRM. They include:

These products are helpful for community planners, but individual property owners can also use them to get a clear idea of their flood risks. Elevation certificates may also be on file with local governments for certain properties. These documents show the elevation of the lowest floor of a building (including the basement) compared to the base flood elevation for the area. An elevation certificate demonstrates community compliance with flood-plain management laws and is used to set appropriate flood insurance premiums. The takeaway A flood can be every bit as catastrophic as a fire. It is worthwhile for property owners to learn their flood risk and take steps to reduce it. Additionally, with the increasing risk of flooding in non-flood-plain areas, if you live near a flood plain, you may want to secure flood insurance.

0 Comments

Leave a Reply. |

Contact Us(281) 815-2003 Archives

October 2023

Categories

All

|

RSS Feed

RSS Feed