Colsa Insurance Agency, Inc. Blog |

|

I remember when one of my children had their one and only accident (thus far – knock on wood) and they called me to inform me. I was expecting a nervous and fearful teen, probably in tears trying to explain me the situation. Surprisingly, it was all the opposite. A calmed, assertive teen, letting me know what had happened, assuring me everyone was ok, and the process they had followed to a T. We had the conversations and process before my children were allowed to get into a car and start driving. Is it any different when it comes to filing Business Insurance Claims? There are many issues that can cause setbacks for businesses. Electrical fires can damage inventory and equipment as well as shut down a business temporarily. Customer injuries can lead to lawsuits, natural disasters can destroy property and burglaries can result in thousands of dollars of losses in equipment and valuables. After any of the above events you'll have to file a claim with your insurer. But if you aren't prepared, take too long to file your claim or fail to document all of your losses, you may not receive a full claims payout. You can avoid that by following these tips (or have processes in place): Gather all Information - Before you file a claim, you have to first understand what happened, because the insurer and your claims adjuster will need detailed accounts of the event and circumstances leading up to it. Look at the insurance policy to see if there are any other necessary steps to take. Some policies include instructions about what to do if certain types of insurable losses occur. Don't procrastinate during this time. It's important that you quickly collect and document all the pertinent information. File your claim with your insurance company - The most efficient way to get your claim started is by contacting the insurance carrier directly. The best way to get the claim underway is by visiting your carrier's website and going through their claims process. Many offer a convenient online method, but also provide an 800 number to call if you prefer to speak to someone one-on-one. Whether you do it online or over the phone, you will be walked through the claims intake process. Be prepared to provide the information you gathered in the first step because your insurance company will need to know all the details about what and when it happened to properly assess your claim. Most insurers will contact you within 24 to 48 hours after you file your claim. Inform US of the claim - Once your claim has been started, it's now time to inform us, your insurance agent. In addition to answering any questions, we can explain your coverage and properly set expectations for what's to come. Additionally, if your claim has any complexity or nuance, we will be able to work with the carrier and/or provide useful advice and guidance. Create an inventory of losses - While you wait for the claims adjuster to contact you or for them to come out to assess the damage, you can work on creating an inventory of your losses. This is essential for providing a clear picture of the loss or damage. Include descriptions of items, their original values and estimated current values. It is also helpful to include a description about the condition of the item before it was damaged. If it is possible to photograph the damaged items, take photos for the insurer. Find copies of any receipts for damaged items. It is also helpful to do a walk-through of the damaged area with a video camera or a cell phone video camera. Videos help show the damage live and from multiple angles. Use them to supplement photo files. Show proof of the loss - Insurers require policyholders to sign sworn statements that show proof of their losses, and the required information must be sent along with the statement. This statement must be made and signed within 60 days of the insurer's first request for it. Make temporary repairs if needed - If temporary repairs must be made to prevent further damage or to protect other assets, they can be completed before the adjuster surveys the property. Do not order any unnecessary repairs. The only types of temporary repairs that should be made are those that will prevent further damage or prevent a possible liability. For example, a temporary roof repair may be necessary to prevent it from collapsing and injuring people, or a broken window may be fixed to prevent rain from coming into a building and causing water damage. Since repairs are included in the settlement, keep receipts for any services and items purchased. For contracted work, obtain two written bids from separate companies before hiring someone. The takeaway - Always stay organized when going through the claims process. Have a process – in writing -- Keep all papers accessible and have information ready in the event that an agent or adjuster calls. When talking to any repair companies or other related parties on the phone, keep track of calls and the reason for the calls. Save receipts for any items that are purchased in relation to the damage. To learn more about what to do during the claims process, give us a call.

0 Comments

Hurricanes can cause a tremendous amount of death and destruction. Longtime residents of coastal Florida, the Carolinas, Texas, Mississippi, Alabama and Louisiana are familiar with the drill - but there are always procrastinators. Hurricane preparedness takes time. Don't leave it to the last minute. Here are some things to keep in mind when a storm is coming:

By understanding these guidelines, you can protect your home as well as you can and keep your family safe. You will also have an easier time getting reimbursed by your insurance company for any damage.  For 2017, private flood insurance statements had to be reported. This was the first time that such information was required to be reported. The Insurance Information Institute released a list of the market's biggest insurance companies offering the coverage based on previously gathered data and they said that over 80 percent of the market share was held by these leading companies. The top company alone held nearly 55 percent. Total premiums written by all companies totaled over $375 million. What is Private Flood Insurance? This type of coverage is available for both residential and commercial properties. The policies cover excess flood and flood peril, and they do not include damages from sewer backups or crop flooding. In the past, only the government offered flood insurance. However, private insurers are becoming more comfortable offering this coverage today because of the following reasons:

Why Private Insurance is a Good Solution After several catastrophic hurricanes over the past decade, the National Flood Insurance Program offered by the Federal Emergency Management Agency took a major financial hit. It is currently billions of dollars in debt. This has also helped open the market for private insurance companies to offer flood protection. Lawmakers like the solution since it will help get the NFIP out of debt faster. In early 2017, the NFIP transferred financial risks totaling $1 billion to private insurers. This was done through reinsurance, which FEMA gained approval for, thanks to the Homeowner Flood Insurance Affordability Act of 2014 and the Biggert-Waters Flood Insurance Reform Act of 2012. More options and competitive pricing are two benefits that an improved private flood insurance market would create. A Peek At Potential Savings KatRisk and Milliman partnered to collect and analyze data from three states that have been affected by catastrophic hurricanes and face higher risks of future damages. The organizations looked at data from Louisiana, Texas and Florida. These three states represent over 55 percent of the NFIP's active policies in the USA. The researchers compared NFIP premiums to several private insurance premium models. Research showed that more than 75 percent of Florida homeowners would see lower premiums with private insurers. More than 90 percent of Texas homeowners would save money, and nearly 70 percent of Louisiana homeowners would see a premium drop. About 70 percent of the Texas homes included in the model would qualify for a premium that is one-fifth of the NFIP's equivalent policy. The ratio dropped to about 45 percent in Florida and a little over 40 percent in Louisiana. However, researchers also found that about five percent of the modeled homes in Texas would see premiums that were higher than the NFIP's, and the ratio increased to about 15 percent in Florida and over 20 percent in Louisiana. As researchers continue to track state-specific data in the coming years, more property owners will be making the switch to save money. To learn more about private flood insurance and if it is a good solution for individual needs, contact us.  Almost everyone has a risk of their home being flooded, regardless of where they live. And now as flooding has become an annual threat to many communities across the country, even areas that were not considered flood-prone are also at risk. There was record rain and snow in many parts of the country in the early part of the year, and many areas can therefore expect flooding. According to the Federal Emergency Management Agency, more than 20% of all flood insurance claims come from areas outside of high-risk flood zones - and that number is rising with each passing year. That still means the vast majority come from high-risk areas. How can a property owner find out what their flood risk is? Gauging your flood risk FEMA considers a property to be at high risk of flood if there is at least a one-in-four chance of flooding during the life of a 30-year mortgage. Geographic areas with this risk are known as special flood hazard areas (SFHAs). Federal regulations require federally regulated or insured mortgage lenders to confirm that mortgaged properties in these areas carry flood insurance. The traditional way to determine a property's flood risk is to locate it on a flood insurance rate map (FIRM). FEMA publishes these maps based on geographic survey data. They are the official depictions of flood hazards in a locality. FIRMs are freely available for review at the Flood Map Service Center on FEMA's web site. As a property owner, you can view your flood risk by entering your address in the search field. Flood maps assign each area in a community to labeled flood zones. Areas with low-to-moderate risks of flooding are assigned to zones with labels beginning with the letters B, C, X or a shaded X. SFHAs are designated with the letters A or V. These areas are shaded on the maps for easy identification. Property owners can also search for their flood risks at FEMA's flood insurance consumer web site, www.floodsmart.gov. By entering your address in the fields on the home page, you can quickly learn whether you face a low-to-moderate or high risk. The site offers other valuable tools, such as an estimator that can calculate how much financial damage a given amount of water (two inches, four inches, etc.) would cause in homes of various sizes. For example, six inches of water in a 2,000 square foot home would cause $39,150 in damage. FEMA also offers a suite of flood risk products that go beyond the information provided in a FIRM. They include:

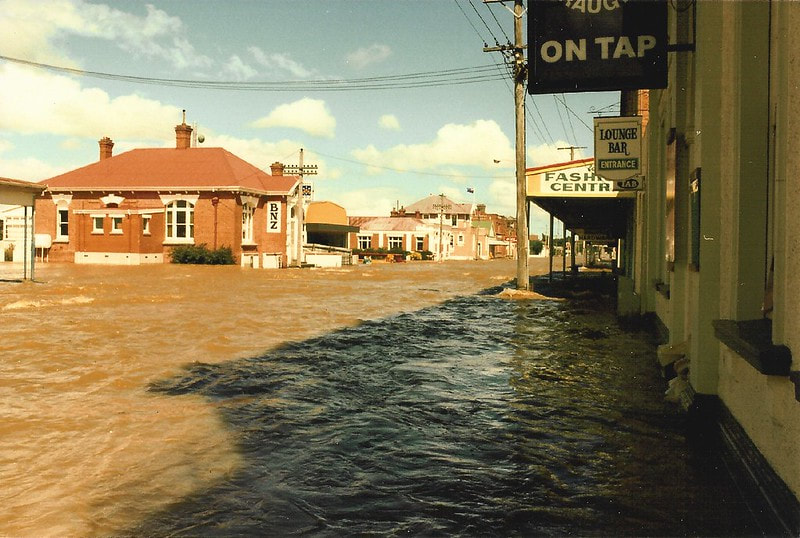

These products are helpful for community planners, but individual property owners can also use them to get a clear idea of their flood risks. Elevation certificates may also be on file with local governments for certain properties. These documents show the elevation of the lowest floor of a building (including the basement) compared to the base flood elevation for the area. An elevation certificate demonstrates community compliance with flood-plain management laws and is used to set appropriate flood insurance premiums. The takeaway A flood can be every bit as catastrophic as a fire. It is worthwhile for property owners to learn their flood risk and take steps to reduce it. Additionally, with the increasing risk of flooding in non-flood-plain areas, if you live near a flood plain, you may want to secure flood insurance.  Parts of the Midwest have experienced record flooding in the spring of 2019, caused by rains and the melting of massive amounts of snow that fell in the winter.

And as the weather becomes more unpredictable, many areas throughout the country are experiencing flooding with increasing regularity. Moreover, some regions are flooding for the first time in recorded history. Floods are the leading weather-related cause of property damage. After Hurricane Sandy, the National Flood Insurance Program paid out well over $6 billion in claims. It is important to take these steps to prevent flood damage. Use flood maps These maps are drawn up and updated by the Federal Emergency Management Agency. They show the locations of flood zones and flood plains, and flood zone risks ranging from high to low. If unsure about the classification of a specific address, ask us. As part of FEMA's modernization program, most communities are receiving new maps with more details and helpful recommendations. Since flood zones may have changed, it is important that you look at the newest versions of these maps. Learn base flood elevation When property owners know their flood zone, they should also learn their property's base flood elevation (or BFE). This is the point where a building has a 1% chance of flooding each year. FEMA's newer maps typically list the BFE for different properties. If new maps are not available yet, your local building department may be able to help. When the BFE is known, it is important to determine the elevation of the first floor of the home. Is it below or above the property's BFE? Raising a structure with a main floor below the BFE helps reduce flood risks. This type of floor plan is typical with some split-level homes and buildings. Purchase flood insurance When you understand the full risk of flooding for your property, you can decide whether you should purchase flood insurance for complete protection. Obviously, if you live in or near a high-risk flood zone, you should purchase coverage. Sometimes you don't have a choice about buying coverage. Most lenders will require homeowners in flood zones to purchase insurance if they want to qualify for a home loan. Flood insurance is mainly available through the National Flood Insurance Program, although there are some private insurers that offer coverage in selected areas. To learn more about your options and how to enroll in coverage, call us. Reduce risks on your property There are several steps to take to reduce risks on the property:

To learn more about flood safety and preparedness, call us. |

Contact Us(281) 815-2003 Archives

October 2023

Categories

All

|

RSS Feed

RSS Feed